Charlie Robertson of Renaissance Capital -

The fastest growing economy in the world last year was Ethiopia. This is symbolic of the global changes that have attracted entrepreneurial investors into frontier markets. The BRICS story is not over, but when three of the component economies are struggling with stagflation and China is slowing, emerging markets no longer attract the same excitement they once did. However, from Pakistan to Kenya, new opportunities for investors have emerged and they may soon be joined by the most exciting opening up since the collapse of the Soviet Union – Iran.

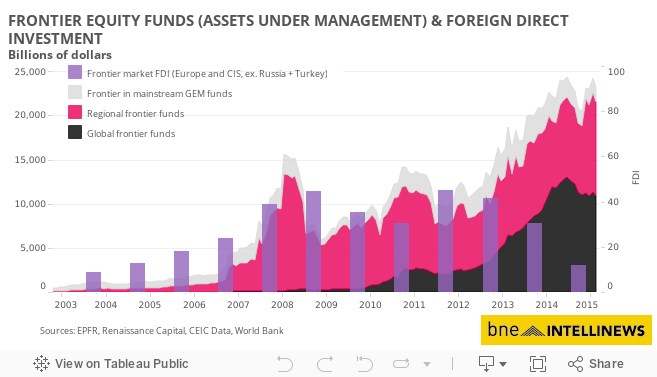

Already frontier markets have seen a boom in equity inflows. There was just $1bn invested in frontier equities in the early 2000s, which rose (and then fell) to $5bn in 2009 and has now rocketed to $25bn. A very few worry this is a bubble – but the $25bn gives exposure to nearly 1bn people (just a few hundred million less than China or India) and around $3 trillion of GDP. It contrasts with nearly a trillion dollars in emerging market equities.

Meanwhile, debt investors have enthusiastically embraced debut Eurobonds from Kenya to Rwanda. The latter’s first issue was hugely oversubscribed, was equivalent to 15% of GDP and yielded 7% in dollars, a figure which roughly matches the country’s real growth rate. We see Rwanda as the Singapore of Africa and buy into the view that its borrowing will help change Rwanda from a largely rural economy to a service-led economy that hosts conferences, tourists as well as offshore back office services.

What we find in frontier markets is some very recognisable development stories that are very familiar to mainstream emerging market investors. Our favourite market this year is Pakistan. Burdened by popular misperceptions that stem more from the TV series Homeland than from any direct knowledge of the economy, most investors have written this country off. Yet we see it as the best undiscovered story in global markets today, and much like Turkey in the 1990s.

While investors have gone overweight on India in the hope that Prime Minister Narendra Modi will deliver reform, we believe investors should be overweight on Pakistan because Prime Minister Nawaz Sharif is delivering reform. His government has nearly halved the budget deficit to 4-5% of GDP, is privatising the banking and electricity sectors and has cut subsidies. Inflation has fallen to 3%, the currency is supported by a nearly balanced current account deficit, interest rates are in single digits, and with less than 12% of Pakistanis owning a bank account, we see huge scope for credit growth in coming decades. GDP growth is accelerating to 4-5%, credit rating agencies are upgrading the country and MSCI has the country on review to graduate from frontier status to emerging market status, which we think will be a 2016-17 event.

Emerging Europe has its frontier stories too – and this is part of the attractiveness of the “asset class”. It is not just countries that now have an educated demographic boom story such as Nigeria or Bangladesh, but it also includes Slovenia, Lithuania or Estonia. Each of the latter group now has the euro as its currency, has relatively high per capita GDP and in Estonia’s case, includes some cutting edge development themes. My latest television interviews with Chinese news, or CNBC Africa, were done via Skype, which was developed in Estonia. Georgia’s 4m people are another fascinating example of what dedication to reform can inspire. This is a country whose bonfire of regulation over the last decade – it is one of the world’s easiest places to do business - has created entirely new export sectors, soaring tourism, and high economic growth.

Romania’s nearly 20mn population is the largest emerging European frontier market. Reformers are in the ascendant here too, and intent on privatising more of the economy and expanding the stock market. President Klaus Iohannis, an ethnic German from that 1% minority of the population, was elected on an anti-corruption platform in a country that has shown remarkable dedication in rooting out corruption even at the highest levels of government. The stock exchange is led by Ludwik Sobolewski, an experienced Pole, who is intent on pushing Romania from frontier status to emerging market status.

Indeed, frontier markets are becoming a conveyor belt, taking somewhat illiquid smaller markets onto the bigger emerging market stage. The stock markets of both UAE and Qatar boomed when they made this shift in 2014 and many (including us) expect to see many more examples of this in coming years.

Of course there are risks. When we argue that many frontier markets look like the emerging markets of 20 years ago, there are some very significant challenges implied by that. In Pakistan, the army has a history of political intervention, just like Turkey until as late as 1997. It was only just over a generation ago, in 1993, that Russian tanks were shelling its parliament building. We put the chances of a coup in Pakistan at about 3-4% a year. The terrorism and conflict experienced by Nigeria or Pakistan again is reminiscent of Turkey’s challenge from the PKK in the 1990s – and did not derail their development. Even now, China is not yet a democracy, even after 20 years. Corruption is a constraint on Russian growth, even after 20 years. And all along the development path, we will see booms and busts, much as we saw in the Asian crisis of the 1990s that engulfed Brazil and Russia too.

Yet these are challenges that experienced emerging market investors have navigated before and are probably better able to manage than at any time in the past. Investors in frontier markets have more scope to hedge or diversify their risks than ever before. Information flow is often better and ever quicker too. The quality and timeliness of statistics out of Kenya is significantly higher than what I could glean from the faxes that Greece’s statistics office would churn through to me in the 1990s.

Frontier markets are not yet mainstream but they will be. When most global emerging market investors own Pakistan or Nigeria – rather than just the adventurous few – we will have returned to the era in the 19th century, when European investors were helping finance the development of emerging markets such as South Africa, Australia, Tsarist Russia and the United States. Frontier markets are here to stay.

Charlie Robertson is chief strategist at Renaissance Capital

Related Articles

Austria's Erste rides CEE recovery to swing to profit in Jan-Sep

bne IntelliNews - Erste Group Bank saw the continuing economic recovery across Central and Eastern Europe push its January-September financial results back into net profit of €764.2mn, the ... more

EU, US partly suspend Belarus sanctions for four months

bne IntelliNews - The Council of the European Union (EU) has suspended for four months the asset ... more

bne:Chart - CEE/CIS countries perform particularly well in World Bank's "Doing Business 2016" survey

Henry Kirby in London - Central and Eastern Europe and the Commonwealth of Independent States’ (CEE/CIS) countries performed particularly well in the World ... more

Most Read

-

Iran presses Afghanistan's Taliban to uphold water-sharing agreement

23 hours ago

-

Romanian consumer protection body begins investigation into Temu and Shein

20 hours ago

-

Don't mention the "D" word - Ukraine

5 days ago

-

Europe unlikely to tackle Russian LNG imports anytime soon

2 days ago

-

EU finally boosts defence investment into arms production as Ukraine runs out of ammo

1 month ago

-

Ukraine's birth rate plummets to 300-year low as country’s population collapses

7 days ago

-

EU finally boosts defence investment into arms production as Ukraine runs out of ammo

1 month ago

-

Fresh evidence suggests that the April 2022 Istanbul peace deal to end the war in Ukraine was stillborn

8 days ago

-

Don't mention the "D" word - Ukraine

5 days ago

-

Europe unlikely to tackle Russian LNG imports anytime soon

2 days ago

-

Russia could pay off its entire external debt tomorrow, in cash

26 days ago

-

Speculation swirls of “Men in Blue” in Crocus City Hall terrorist attack linked to FSB

30 days ago

-

Albanians campaign on social media to keep bus bridge created in freak accident

1 year ago

-

BRICS announce a blockchain-based payment system to create a common currency

28 days ago

-

Saudi Arabia to scale back plans for Neom city

15 days ago