Henry Kirby in London -

Standard & Poor’s downgrade of Russia to junk status on January 27 was met by the Kremlin with accusations of US-influenced politicking. Russian news agency RIA Novosti quoted Deputy Foreign Minister Vasily Nebenzya as saying that he has “no doubt that this was done not even on the prompting but on direct orders from Washington”.

While there is little argument that 2014 proved to be a damaging year for the Russian economy, a closer look at some basic macroeconomic figures would offer some credence to the Kremlin’s cries of foul play – especially when compared to other economies still ranked investment grade.

S&P’s main justification for downgrading Russia to ‘BB+’ – its highest non-investment grade – was the country’s newfound lack of access to international capital markets. The implicit message there is that, in the not-too-distant future, Russia simply will not be able to service its debt obligations.

The widely used metric of public debt as a percentage of GDP is seen as a broadly reliable indicator of a country’s level of indebtedness. A glance at the bne:Chart below reveals not only how healthy Russia is in this respect, at 9.2% of GDP, but also the comparative fragility of other nations – including those whose sanctions led to the S&P downgrade.

Without access to capital markets, Japan would have to use more than two years’ total GDP to service just a single year of public debt. Russia, on the other hand, could pay its own off with little more than a month of output.

Even this measure fails to take into account that governments do not have their countries’ entire GDP as a liquid fund for servicing debt, but only the product that comes back to it in the form of tax revenues.

Looking then at tax revenue as a percentage of total public debt, the picture is even bleaker for the highly-indebted developed countries (HIDCs), as the second bne:Chart shows. It would take the US over three years of real income to service a year of public debt and Japan over seven years. Russia’s tax revenue, however, would cover its obligations twice over in a single year.

Taking the hypothetical scenario to the extreme where the Russian economy ground to a halt, its only buffer would be its reserves. With no other source of capital, it would have no option but to dip into its coffers to bankroll the material needs of the nation and service its debt obligations with its own cash. Even in this extreme case, Russia is set up to withstand a worst-of-the-worst scenario for a surprisingly long time.

As the third bne:Chart shows, the Central Bank of Russia (CBR) could cover just shy of two years’ worth of debt obligations with its reserves. The US Federal Reserve, on the other hand, could cover just three days’ worth of debt and would run out of funds shortly after lunchtime on day four.

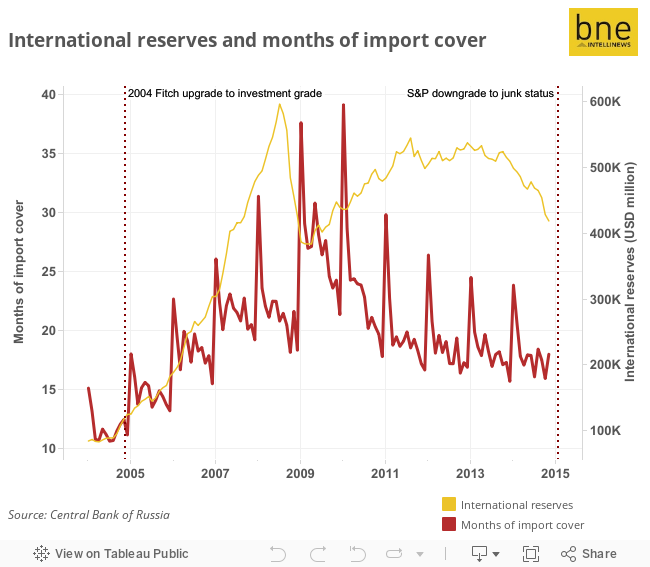

Curiously, a look back at the CBR’s historical reserve levels shows that, in terms of import cover, Russia is actually healthier now than it was when ratings agency Fitch upgraded it to investment grade in 2004.

While these scenarios go some way to illustrating the robustness of the Russian economy, they do not factor in the high, and growing, levels of inflation that Russia is suffering – 11% at the time of writing. This alone would shorten Russia’s lifeline considerably. Conversely, though, the scenarios also work off of the assumption that Russia’s access to capital markets has dried up completely as a result of sanctions, which is not the case.

Use the bne:Chart below to compare Russia with other countries across a number of economic indicators

Related Articles

Drum rolls in the great disappearing act of Russia's banks

Jason Corcoran in Moscow - Russian banks are disappearing at the fastest rate ever as the country's deepening recession makes it easier for the central bank to expose money laundering, dodgy lending ... more

Kremlin: No evidence in Olympic doping allegations against Russia

bne IntelliNews - The Kremlin supported by national sports authorities has brushed aside "groundless" allegations of a mass doping scam involving Russian athletes after the World Anti-Doping Agency ... more

PROFILE: Day of reckoning comes for eccentric owner of Russian bank Uralsib

Jason Corcoran in Moscow - Revelations and mysticism may have been the stock-in-trade of Nikolai Tsvetkov’s management style, but ultimately they didn’t help him to hold on to his ... more

Most Read

-

EU finally boosts defence investment into arms production as Ukraine runs out of ammo

1 month ago

-

Europe unlikely to tackle Russian LNG imports anytime soon

1 day ago

-

Unstable dams mean Chernobyl-scale nuclear disaster threatens Central Asia’s Fergana valley

19 hours ago

-

Will the Baku-Supsa pipeline become Azerbaijan's second oil export artery?

5 days ago

-

COMMENT: Can China compensate for Russia’s losses on the European gas market?

1 day ago

-

Ukraine's birth rate plummets to 300-year low as country’s population collapses

7 days ago

-

Fresh evidence suggests that the April 2022 Istanbul peace deal to end the war in Ukraine was stillborn

7 days ago

-

EU finally boosts defence investment into arms production as Ukraine runs out of ammo

1 month ago

-

Russia’s war economy boosted by rising oil prices

8 days ago

-

Russia’s $13.4bn current account surplus in March second highest since 2007

7 days ago

-

Russia could pay off its entire external debt tomorrow, in cash

25 days ago

-

Speculation swirls of “Men in Blue” in Crocus City Hall terrorist attack linked to FSB

29 days ago

-

Albanians campaign on social media to keep bus bridge created in freak accident

1 year ago

-

BRICS announce a blockchain-based payment system to create a common currency

27 days ago

-

UBN: Russia could take the Baltic states in 48 hours

1 month ago